RBI has announced yet another revolutionary milestone in the digital payment journey of India. CBDC or the Central Bank Digital Currency is bound to shake the proverbial branches of the economy. Based on blockchain ledger technology and introduced as a challenger to infamous cryptocurrencies like Bitcoin and Ethereum, it shall serve as a complement and perhaps in the long run an alternative to cash.

Before understanding what CBDC is, however, we need to understand what currency is. Currency is a medium of exchange that acts as a standardized token for payment of goods and services. This includes basic amenities like food and water, and luxury goods like expensive cars and jewelry. The journey of payments started thousands of years ago with the barter system which slowly but surely was replaced by token currency. In medieval times, token papers with the king’s or the issuer’s stamp could be exchanged for goods or for other token currency like gold, silver, or even copper coins. The longevity and the impervious nature of noble metals like gold and silver made them naturally viable options for making coins. With time however cash currency was introduced mainly due to the difficulty in handing and transporting coins.

Gradually paper currency became a natural evolution of coins. What token currency means is that its value lies not in itself or its material but the promise that it bears. You might have noticed that every Indian currency note contains a promise from the RBI governor alongwith his signature, stating that its bearer shall receive the sum of money mentioned on the cash note. CBDC runs on the same token value concept. It is a legal tender that is backed by a promise from the RBI or the Reserve Bank of India about its value and most importantly its authenticity.

How is CBDC Different From Cash?

Existing exclusively on digital platforms, CBDC is based on blockchain ledger technology, which means that with this digital coin you won’t receive a tangible token like cash that you can then exchange with merchants or other retail users. It will be distributed as well as exchanged on digital platforms only. RBI and NPCI has currently chosen a handful of banks for its pilot phase and only through the platforms of these banks, the CBDC token can be “withdrawn”.

Another important distinction between cash and CBDC is that every token however small in denomination will have the full history of transactions done using that token. Cash holders have anonymity in the sense that you can’t possibly know from which ATM a certain 200 rupee note was withdrawn and how many hands it has exchanged before reaching you. With CBDC this is possible.

Due to blockchain alogrithm and smart contract technology you can know where a certain token was generated and how many and what type of transactions have been performed using it since then. Though it raises a privacy concern this feature also provides the central bank and regulatory authorities a way to track illegal activities and money laundering. Money laundering infact would be virtually impossible with CBDC.

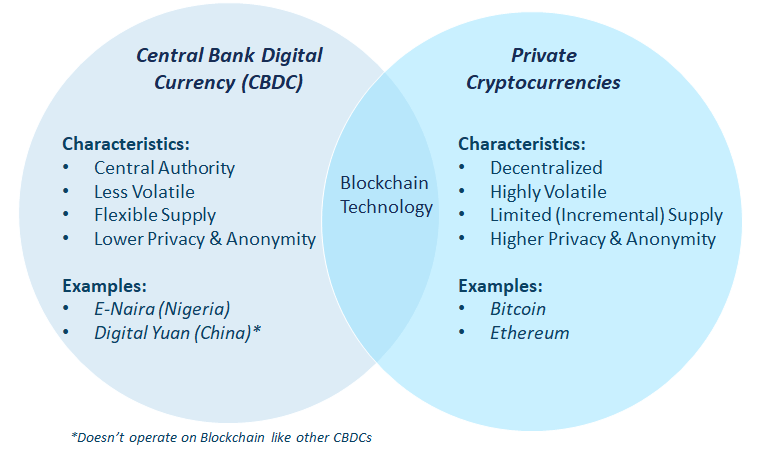

CBDC Vs Cryptocurrency

CBDC although based on the same blockchain ledger technology as famous cryptocurrencies like Bitcoin and Ethereum has a very important difference from them. CBDC is not decentralized. This essentially means that the Digital currencies like Chinese Digital Yuan and India’s CBDC are governed, regulated and maintained by a center authority which in India’s case is the Reserve Bank of India. In other countries like US and Nigeria similar Central Bank digital coins have been already successfully launched.

By virtue of being centralized the value of a digital coin doesn’t change. So, if you have a 100 INR token in CBDC it won’t change value like Bitcoin does. Bitcoin on one day is 35000 USD but on other days it might come down to 10000 USD. But CBDC of India will retain its value simply because its value doesn’t depend on market sentiments. Cryptocurrencies in this respect behave like stock and mutual funds because their value is based not on a predefined criteria but on the supply demand gap of an open market.

Privacy Concerns of Digital Coins

As I mentioned, customers may have some concerns in using CBDC especially because it can tell you the exact purpose for which a certain token was exchanged. Even if not to the end customer but definitely to the regulatory authorities and the police. Infact there is no inherent customer benefit in CBDC that UPI or other digital payment instruments are not providing. The settlement of digital coin would be in real time but that doesn’t affect the customer rather the banks, NBFCs, and merchants involved in the transaction. How the customers will react to these privacy concerns remains to be seen at this point.

How Will CBDC Work?

- The denominations of the digital coin would be same as current INR cash except that it will have an additional 50 paisa token also.

- All CBDC tokens will have serial numbers and the signature of the RBI governor just like cash notes.

- Tokens will be circulated and distributed to retail customers through mobile app provided by RBI.

- In pilot phase, banks like State Bank of India, ICICI Bank, HDFC Bank, IDFC and others have been approached to go live with the CBDC.

- Benefits of CBDC include reduced dependency on cash, low credit risk for customers, cross border payments innovation, efficient settlement of payments and many others.

- Concerns include implementation constraints, privacy concerns, and end user resistance.

- RBI might also introduce wallets or allow tokens to be stored in and redeemed from wallet apps like Paytm, Phonepe and GPay in subsequent phases but that is not clear at this point of time.

Some Similar Articles

Siddhu Moosewala Was More Than A Singer: He Was A Legend

Our country is full of nepotism infested superstars. They are only known to the public because their father or mother…

Keep reading

Flexible Work Timing is the Future

The Hype of Flexible Working All articles nowadays have to compulsorily contain a couple of keywords: Corona, COVID-19, Russia-Ukraine conflict,…

Keep reading

Why Every Millennial Wants to Leave His Job?

No Respect for Employees The biggest problem of today’s job arena is that it has no respect for anyone it…

Keep reading

6 Tricks to Achieve Better Work-Life Balance

6. Understand What is ‘Not’ Important The first step to separating your work and personal life is to identify what…

Keep readingSomething went wrong. Please refresh the page and/or try again.

Leave a comment